EHLS: Outperforming Since August Lows

- Jun 9, 2025

- 4 min read

Updated: Jun 29, 2025

Despite Sharp Market Gyrations

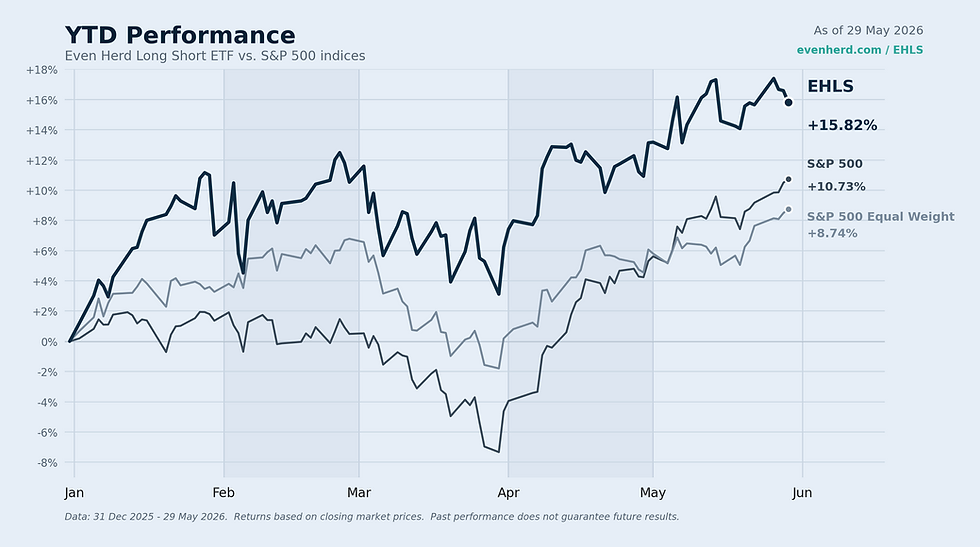

The chart reflects market prices ("MKT"). The fund’s expense ratio is 1.58%, which includes estimated dividends and interest expense on short positions. If this were excluded, the expense ratio would be 1.15%. The fund's inception was 4/2/2024. The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when sold or redeemed, may be worth more or less than their original cost, and current performance may be lower or higher than the performance quoted. For standardized performance, visit https://www.evenherd.com/ehls.

In This Update

Clustering Validated: EHLS has outperformed the S&P 500 by over 3% and the equal-weighted S&P 500 by more than 6.5% (MKT) since fully implementing updated clustering on April 1st.

Financials and Utilites remain in lead: The fund continues to exhibit strength in Financials and Utilities, while Healthcare and Energy remain underweight.

International Strength: Regional volatility persists in markets like Argentina and China, but select international banks held in the portfolio are near all-time highs.

Volatility Assumed: Market volatility is expected to remain elevated amid tariff discussions and rising global interest rates.

50% Net Equity: EHLS is maintaining approximately 50% net equity exposure heading into June.

Looking Back

Market headlines continue to drive daily volatility, yet we’re encouraged by the fund’s performance—having outpaced the S&P 500 by more than 4% since its August low of last year. In our previous update, we highlighted meaningful enhancements to our clustering methodology, aimed at better synchronizing long and short positioning. Since the full implementation of these updates on April 1st, EHLS has outperformed the S&P 500 by over 3% and surpassed the S&P 500 Equal Weight Index by more than 6.5%.

The most notable challenge during this year, which we previously wrote about, occurred over the five trading days following February 18th. We believe the improved clustering process will help mitigate such instances moving forward. Encouragingly, even with that drawdown, the fund captured less than half the downside experienced by the S&P 500 during the volatile early weeks of April—demonstrating our objective of upside participation with reduced drawdown sensitivity.

Throughout the month, Financials and Utilities maintained overweight status and continued to show strong relative performance. Regional exposures, particularly in Argentina and China, contributed to heightened volatility, yet several international banks—such as HSBC, NatWest Group (NWG), and Mizuho Financial (MFG)—remained resilient, with many reaching new highs.

Looking Forward

We anticipate Financials and Utilities will remain overweight as we move through June. The broader sector landscape, however, remains mixed, with Healthcare and Energy ranking lowest and expected to stay underweight. Given how closely many sectors are currently ranked, some rotation in relative weightings is likely throughout the month.

Market volatility is likely to persist as geopolitical developments—especially tariff commentary—continue to sway investor sentiment. While economic indicators have been mixed, the overall tone has skewed positive despite continued uncertainty, and potential stabilization in inflation is being observed on the backdrop of survey expectations pointing to the inverse. A sharp move higher in global interest rates has introduced additional uncertainty, particularly for companies with elevated leverage. While macroeconomic factors are not core to the fund’s process, we remain attuned to evolving trends that could indirectly affect relative performance.

Although the swift and overextended April drawdown suggested rising near-term risk towards the upside instead, we refrain from making directional calls. That said, evidence points to a renewed interest in growth-oriented exposures, creating an interesting contrast with Utilities’ continued leadership. Momentum names that shown bright before the market correction have mostly found their ways to new highs, such as Palantir (PLTR), Carvana (CVNA), Sprouts Farmers Market (SFM), Robinhood (HOOD), among others. Within the Utility sector, we observe that leadership is increasingly tied to AI and deregulation-driven themes—exemplified by holdings like Vistra Corp (VST), NRG Energy (NRG), and newly added Korea Electric Power (KEP), which reflects strong international utility momentum.

We’ll continue to monitor and report on material sector shifts in upcoming updates. For now, Financials and Utilities remain areas of strategic focus, with the fund expected to maintain its average net equity exposure of approximately 50% throughout June, although this could fluctuate.

Comments