EHLS: Strong Market Gains Continue

- Sep 5, 2025

- 5 min read

Strength Seen from the Bottom Up

In This Update

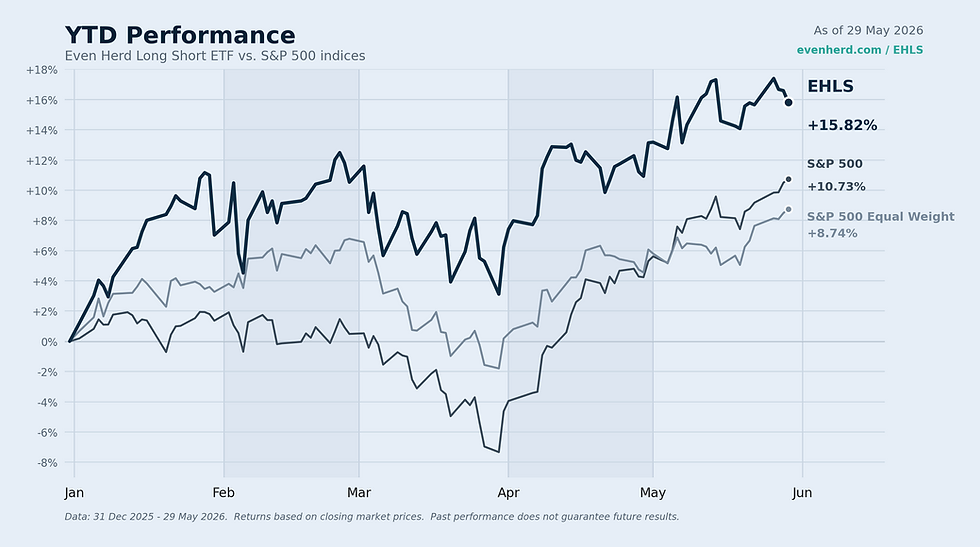

Market Recovery and Volatility: The market has shown resilience, rebounding from a steep April decline with notable strength in lower-ranked stocks.

Industry Performers: Tobacco stocks continue to lead Consumer Defensive gains, while gold miners and independent utility operators remain strong for the year within our system.

AI Theme Resilience: The AI-driven investment theme regained momentum after a February-March dip as discussed in July’s update, though it faced volatility at month-end.

Portfolio Strategy: The fund maintains overweight positions in Financials, Utilities, and Industrials, which should continue through September.

Underweight Sectors: Energy and Real Estate, particularly REITs, remain underweight, with Welltower Inc. (WELL) as the top-ranked REIT but still lower in overall rankings.

Looking Back

The market has continued its upward trajectory with extreme strength seen in some of the worst-performing stocks, or from the bottom up as we would say, observed in part of last month and again in August, characterized by significant daily volatility. When we segmented our system into thirds based on our proprietary rankings, we found the bottom third of stocks outperformed the top third by a factor of four on certain days in August. Such dynamics are rare and typically observed post-recession or crisis, as last seen in late 2020. However, this year’s market behavior does not align with those conditions, as the sharp decline in April was followed by the fastest recovery on record with no recession triggered, signaling robust market depth and strength, especially in speculative trades. We would anticipate this kind of behavior to moderate moving forward but will conitnue to monitor any developments.

Because of the strength in previously poor performers, managing short positions targeting that group in this environment has proven challenging, contributing to a significant drag on the fund’s strong long portfolio performance this month. We aim to prioritize upside participation over purely downside preservation, so a deviation in that setting is frustrating, although not unprecedented. Despite ongoing claims of a market bubble, we believe if the market is in any such bubble, it is far from its peak, a topic we will explore in a potential upcoming “Observing the Herd” article. That theory hinges on seeing this kind of strength in the depth of our system, which alleviates any imminent recessionary concerns. However, we believe our theory is more founded in what we observe among many of the AI-related companies. Given the inherent momentum-nature of some of, primarily, the long positions, we would not be surprised to see volatility persist as the market continues to weigh the potential upside in the AI-related businesses, which we see as the broadest theme impacting the most amount of publicly traded businesses since the dot-com bubble.

The AI investment theme, which suffered considerably during the February-March momentum crash, continued to gain momentum this month, as has been observed and previously discussed in past updates. We remain optimistic about the long-term potential of this theme, guided by our systematic approach to maintain exposure. In other sectors, independent utility operators and gold miners continue to vie for leadership. The fund maintains significant exposure to gold miners, including Kinross Gold Corp. (KGC), Agnico Eagle Mines Ltd. (AEM), and Alamos Gold Inc. (AGI), offset by a short position in Seabridge Gold, Inc. (SA), which is our highest-ranking short and not one that would be typically held. To diversify within this space, we hold positions in Sprott Inc. (SII), a financial asset manager, as well as Skeena Resources Limited (SKE), Perpetua Resources (PPTA), and MAG Silver Corp. (MAG) in related mining industries.

Looking Forward

Closing the month at just under 54% net equity exposure, we would intend to maintain roughly this level of exposure through the month, plus or minus five percent. While we do not have any near-term recessionary concerns and do expect the Fed cut this month, we are hopeful market trends resume, providing ample opportunity on both the long and short side of the portfolio. Financials continue to lead as an overweight sector in the fund, followed closely by Utilities and Industrials, a trend we expect to persist through September absent significant market shifts, particularly in the AI theme. Within Utilities, independent providers like Vistra Energy Corp. (VST) and NRG Energy Inc. (NRG) remain top-ten holdings and are expected to maintain their rankings, which tend to correlate with the theme as well.

Energy and Real Estate remain the most underweight sectors with Healthcare close by. Real Estate, particularly REITs, offers limited investment opportunities within our top 500 stocks but presents ample shorting options, which we keep limited due to minimal long exposures. Consequently, Real Estate closed the month as the only sector with net negative exposure, a position we will monitor closely. Within Real Estate, Welltower Inc. (WELL), a healthcare-focused REIT, ranks as the highest REIT but remains outside the top 350 in our system. Because of this, we're generally unable to gain any meaningful exposure to the sector currently. Also of note, the Hotel & Motel industry continues to underperform, ranking as the lowest REIT category, surprising given the recent resilience in Leisure & Hospitality labor market data.

The extreme volatility observed earlier this year, with AI-related and other momentum-favorable stocks fluctuating over 50% from February to April, underscores the need for smoother market conditions to foster sustainable trends. As we enter September, our focus remains on continuing to selectively broaden gross exposures to dampen cluster-driven drawdowns while maintaining disciplined management, guided by our proprietary system. While we expect the AI-theme to continue with names like Broadcom (AVG) and Celestica (CLS) among others, we follow the guidance of our system, which will eventually force us away from any exposure when that day does come and the theme turns into a longer-term underperformer. As mentioned previously, we do not believe that day is close, yet, but feel comfort knowing we have a systematic approach to guide the fund when the time comes. For now, we're optimistic for sustainable trends to resume after witnessing months of market gyrations in specific niches, causing jarring moves across individual equities beyond typically observed volatility.

Comments