EHLS: Double-Digit Performance YTD

- Mar 3

- 6 min read

Even While Momentum Struggles

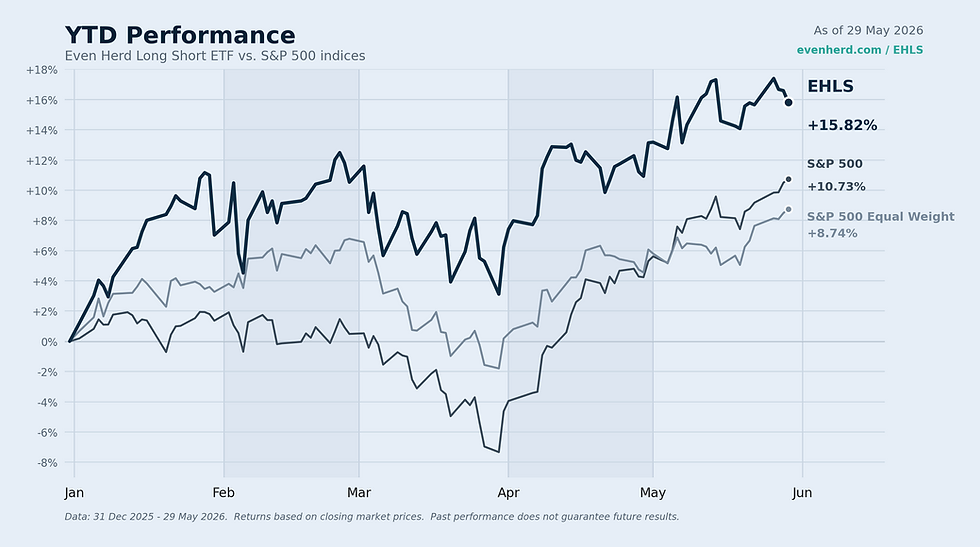

Year-to-date, the fund now stands at +10.52% (MKT) compared to the S&P 500 at just +0.49%, a double-digit relative advantage through only two months. We are pleased to report a continued strength in February as the fund gained +3.23% (MKT), while the S&P 500 declined approximately -0.4% for the month. This outperformance has been driven by a combination of structural positioning in precious metals and materials, an improving Energy allocation, disciplined net exposure management, and a short portfolio that benefited from the ongoing repricing of legacy software businesses.

Diversification across clusters, industries, and individual securities remains central to portfolio construction and is guided by our proprietary system. The fund ended February at 57.33% net equity exposure, down from recent months, as we continue to prioritize volatility management heading into what we expect will be a more turbulent period for broader markets.

The chart reflects market prices (MKT). The fund's expense ratio is 2.62%, which includes estimated dividends and interest expense on short positions. If this were excluded, the expense ratio would be 1.15%. The fund's inception was 4/2/2024. The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when sold or redeemed, may be worth more or less than their original cost, and current performance may be lower or higher than the performance quoted. For standardized performance, visit https://www.evenherd.com/ehls.

IN THIS UPDATE

• Precious metals continue to anchor the portfolio, with gold approaching $5,300 and silver reaching $92 per ounce during the month, extending one of the most powerful trends in recent memory. |

• Tax-efficient redemptions were executed in select positions including Agnico Eagle (AEM), Skeena Resources (SKE), and Sprott Inc. (SII) to manage concentration following outsized appreciation. |

• Energy has risen to the third-strongest sector in the system, behind only Materials and Utilities, marking a notable improvement in relative strength. |

• Communication Services and Consumer Discretionary have been the largest drags in the system during February, and exposure remains light. |

• The fund reduced net equity exposure to 57.33%, with an expected near-term range of 55 to 65%. |

LOOKING BACK

PRECIOUS METALS: STRENGTH PERSISTS

The precious metals complex remained the dominant theme in the portfolio and within the system itself. Gold prices consolidated near record highs, approaching $5,300 per ounce by month-end, while silver continued its remarkable run, touching $92 before pulling back slightly. Precious metals miners, which have maintained the widest leadership gap in the system for several months now, again drove the majority of the fund's outperformance.

Given the magnitude of appreciation in several names, we executed tax-efficient redemptions in Agnico Eagle (AEM), Skeena Resources (SKE), and Sprott Inc. (SII) during the month. Agnico Eagle has returned roughly +48% year-to-date, posting record free cash flow of $4.4 billionin 2025 while raising its dividend 12.5%. Skeena Resources has gained over +57% year-to-date, which benefited from its Eskay Creek project advancement and recent inclusion in the S&P/TSX Index. Sprott hit a new 52-week high of $163.72 in late February after reporting earnings that crushed estimates, $1.11 per share versus the $0.53 consensus, as its precious metals and critical materials AUM surged. These trims are consistent with our approach of ensuring no single position becomes an outsized concentration within the portfolio, while the system continues to support the broader precious metals theme.

MOMENTUM FACES BROADER CHALLENGES

It is worth addressing the wider environment for momentum strategies, as the factor has faced notable headwinds since peaking around September and October of last year. Many popular momentum products, including widely followed ETFs, have failed to reclaim their highs from that period. Quant hedge funds experienced their worst drawdowns since October in the opening weeks of 2026, driven by crowded positioning in U.S. equities and sharp factor reversals. The MSCI USA Momentum Index was up only roughly +2% year-to-date through late February, a stark contrast to what momentum delivered in the prior year.

This environment underscores the distinction between narrow, traditionally constructed momentum strategies and the diversified approach the fund employs. Where conventional momentum products tend to concentrate heavily in recent large-cap winners, often loaded with technology and growth exposure, our system diversifies across clusters, sectors, and individual names while incorporating a meaningful short portfolio. The result has been a portfolio that continues to capture momentum's upside in areas like precious metals and energy infrastructure, while avoiding the worst of the factor's crowding-driven reversals in areas like software and mega-cap technology.

SOFTWARE REPRICING CONTINUES

As discussed in our previous update, the structural repricing of legacy software businesses has only accelerated. The Nasdaq Composite fell approximately -2.5% in February, its worst month since last March, largely driven by continued declines across software and SaaS names as AI disruption narratives intensified. The short side of the portfolio continued to contribute positively from this trend.

The thesis articulated in the last update remains unchanged and was further exapnded upon in our latest "Observing the Herd" article: artificial intelligence is becoming the operating system, not just another application. Software that was once priced for perfection now faces structural uncertainty around growth, as the barriers to building functional software logic collapse. The market's shift in premiums away from asset-light digital businesses and toward physical, tangible assets, such as energy, materials, and infrastructure, continues to play directly into the fund's positioning.

LOOKING FORWARD

VOLATILITY MANAGEMENT REMAINS THE PRIORITY

Heading into March, we remain focused on continuing to manage volatility, which has benefited the fund meaningfully this year but been unusually since inception. Reducing net equity exposure to 57.33%reflects this priority as well as observed declines in our "sea level" or breadth indicator discussed in previous updates, and we expect the range to remain around 55 to 65% in the near term. Given the magnitude of moves in precious metals and the broader uncertainty across technology, tariff policy, and geopolitics, we believe maintaining a disciplined exposure level is prudent even as the system continues to identify compelling long opportunities.

SECTOR POSITIONING

Materials and Utilities remain the top two sectors in the system. Materials continues to be driven by the powerful precious metals mining cluster, while Utilities benefit from the AI-driven power demand narrative and their role as critical infrastructure providers for the data center build-out.

Energy has seen the most notable improvement in relative strength, now occupying the third-strongest sector position in the system. The sector has been the S&P 500's leader in 2026, gaining roughly 14 to 18% year-to-date depending on the measure, driven by the convergence of AI power demand, geopolitical tensions, and strong capital discipline among producers. We expect to maintain or modestly increase exposure as the trend develops.

On the underweight side, Communication Services and Consumer Discretionary have been the largest drags in the system during February. Consumer Discretionary weakness was exemplified by severe declines in names like Amazon following disappointing forward guidance, while Communication Services struggled amid the broader AI disruption repricing. Exposure to both sectors remains light, and we do not anticipate a meaningful increase unless rankings materially improve.

THE BROADER OPPORTUNITY

The challenges facing traditional momentum strategies create an interesting backdrop. When factor-driven positioning becomes crowded and undergoes reversals, it tends to create dislocations that more diversified, systematic approaches can exploit. Our system does not chase the same names as conventional momentum products. It identifies relative strength across a much broader opportunity set, including areas that are often underrepresented in mainstream factor indices.

As always, the system, not our opinion, will dictate positioning. With heightened geopolitical tensions following the recent events involving Iran and the broader Middle East, we are closely monitoring potential impacts on energy markets and risk sentiment. Regardless of how events unfold, our approach remains unchanged: stay diversified, manage exposure thoughtfully, and let the strongest themes compound while cutting positions when rankings deteriorate.

The Even Herd Long Short ETF (EHLS) is a relative momentum-driven long/short equity strategy. For more information, visit evenherd.com/ehls. For the latest from our CEO, read the recent Observing the Herd article: AI: The Future Operating System.

Comments