EHLS: Delivering a Postive First Half

- Jul 2, 2025

- 5 min read

As Geopolotics Disrupts Markets

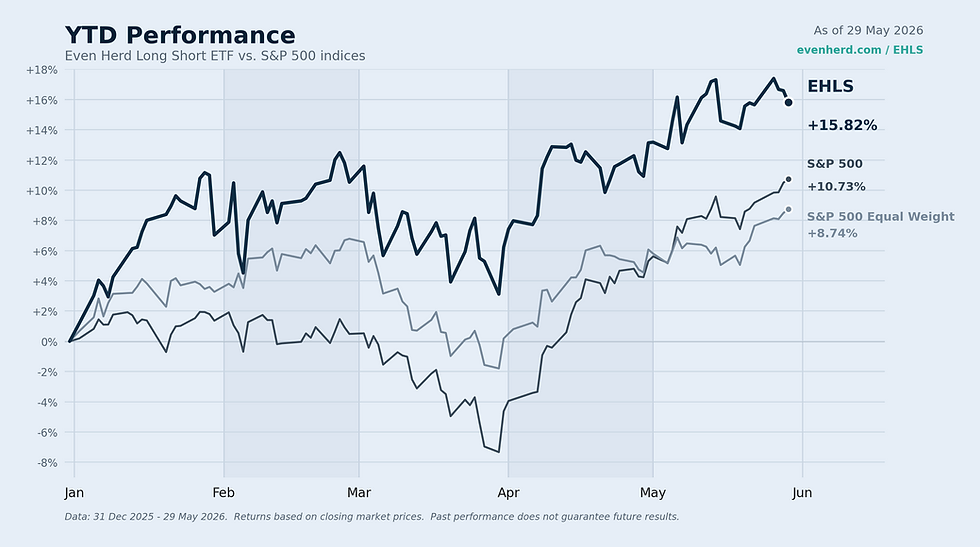

The chart reflects market prices ("MKT"). The fund’s expense ratio is 1.58%, which includes estimated dividends and interest expense on short positions. If this were excluded, the expense ratio would be 1.15%. The fund's inception was 4/2/2024. The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when sold or redeemed, may be worth more or less than their original cost, and current performance may be lower or higher than the performance quoted. For standardized performance, visit https://www.evenherd.com/ehls.

Despite market gyrations, the fund posted a positive first half of the year. Since the market low on August 6, 2024, seen in the chart above, EHLS continues to outperform, gaining 21.50% (MKT) versus 19.64% for the S&P 500, and nearly doubling the return of the S&P 500 Equal Weighted Index (the S&P 500 where all stocks have the same weighting), which gained 11.73% — all while ending June with just 48.22% net equity exposure.

In This Update

Strength Continues: EHLS (MKT) has outperformed both the S&P 500 and its equal-weight counterpart since the August 2024 low.

Gains Despite Shorts: Net equity exposure remains disciplined, ending June at 48.22%, but still capturing ample upside.

Risks of War: Geopolitical events caused sharp but contained market reactions, with volatility short-lived.

Sector Shakeups: Utilities at risk of losing its top two sector spot this month. The fund continues to follow system signals, maintaining a cautious stance on Real Estate and select regions.

Robinhood Announcement: On June 30th, HOOD made one of the most significant announcements in terms of the future of the markets, in our opinion.

Looking Back

June was marked by a major geopolitical shock as Israel and Iran exchanged direct attacks, culminating in a U.S. strike on an Iranian nuclear facility. While Energy briefly strengthened in our system, it reversed sharply as WTI crude fell over 15% in two days. Equity volatility remained subdued, with the VIX (an index measuring the expected 30-day volatility of the S&P 500 based on options prices) briefly touching 22, which could be considered incredibly low for such a significant event. Utilities sector dropped sharply late in the month but retained relatively high rankings. Consumer Defensive and Real Estate also saw steeper declines. Semiconductors rebounded, leading the fund to add exposure to names like Broadcom (AVGO) and Nvidia (NVDA) again. Technology and Communication Services continue to improve, while Financials held the top sector position.

Regionally, Argentina experienced one of its largest system declines since mid-2024. We have begun trimming exposure and are monitoring for further weakness. While no short positions are currently held, additional declines could lead to shorts, though this is unlikely in July unless the downtrend accelerates. Argentina remains one of our more exposed regions due to the lack of poorly ranked stocks available to short — though overall exposure remains modest given our focus on broad diversification. At the lowest cluster level, the fund holds 2.52% net equity exposure to a cluster primarily comprising Argentinian stocks, representing about 5% of total net equity exposure. In strong clusters without offsetting shorts, we are comfortable leaning in and holding net exposure, while closely monitoring these positions.

One of the fund’s top performers in the first half of the year was Robinhood Markets (HOOD), closing up +151% year-to-date (YTD). We previously highlighted the stock’s volatility in February, when it peaked at +75% (YTD) before dropping to nearly -10% in April for the year. Since then, it has more than doubled. HOOD has consistently ranked among the top stocks in our system since February 2024. On June 30th, the stock jumped over 12% in a single day following its presentation on the tokenization of stocks — an event we believe every financial professional should watch closely. It has the potential to dramatically impact trading and markets over the next decade, if successful and allowed by regulators.

Looking Forward

With Utilities potentially in decline in our rankings, Financials are expected to hold the top spot in July. Utilities, Industrials, Technology, Basic Materials, and Communication Services follow as second-tier sectors deserving more exposure than remaining sectors. Real Estate remains firmly underweight — only 5 of 182 tracked stocks rank in our system’s top 500. Given the asymmetric return profile — with long positions offering unlimited upside and shorts capped — the fund typically seeks to keep gross short exposure low in sectors exhibiting this kind of skew to avoid misalignment if conditions unexpectedly shift.

Tariff negotiations, with Canada and the UK recently announcing potential deals being imminent, could drive headlines again, just as trade talks did in April. Geopolitical risks are oddly missing from headlines after such a significant event, but these risks may re-emerge. However, we continue to focus on system cues rather than attempting to anticipate such events. The market trend appears upward for now, continuing to push more speculative names higher, which we discussed in our April update when the market continued to show signs that risks were to the upside.

We expect to maintain around 50% net equity exposure through July, consistent with levels since April. Our enhanced clustering methodologies remain a focus, as they have helped reduce short-term volatility. That said, given the system’s inherent momentum exposure, we still see occasional outlier days when sharp market rotations — seemingly buying declining stocks and selling those at highs — temporarily impact performance. While we continue refining these methods, our priority remains capturing upside to serve as a true equity alternative.

Comments