EHLS: Strong Performance Through Trade War

- May 2, 2025

- 5 min read

Updated: Jun 29, 2025

Fund Gained During Market Volatility

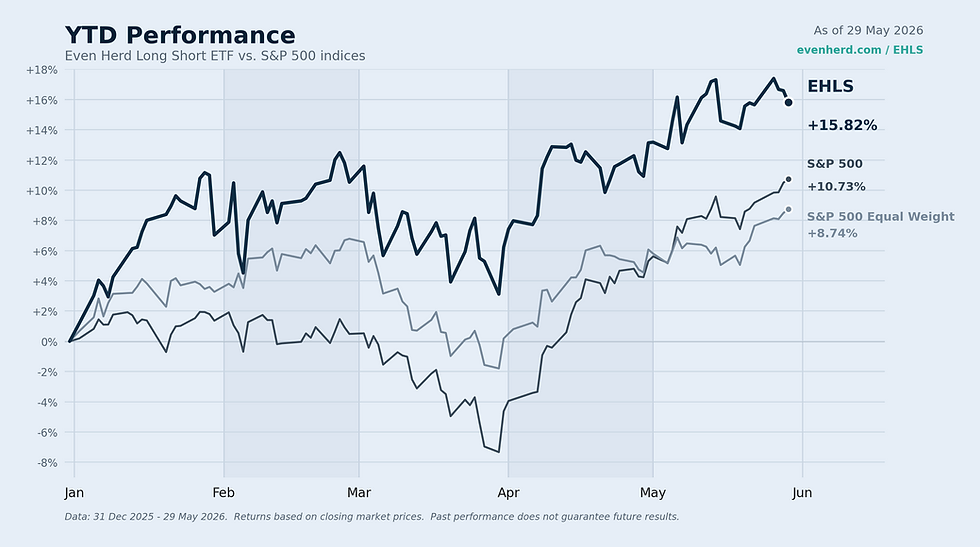

The chart reflects market prices ("MKT"). The fund’s expense ratio is 1.58%, which includes estimated dividends and interest expense on short positions. If this were excluded, the expense ratio would be 1.15%. The fund's inception was 4/2/2024. The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when sold or redeemed, may be worth more or less than their original cost, and current performance may be lower or higher than the performance quoted. For standardized performance, visit https://www.evenherd.com/ehls.

In This Update

Strong Month: EHLS (MKT) outperformed the S&P 500 by 4.68% this month, gaining 3.54% compared to a -1.14% decline in the index.

Shorts Aided: The short side of the portfolio effectively mitigated extreme market volatility, as the VIX spiked to levels comparable to the financial crisis and pandemic.

Tariffs Paused: The 90-day tariff pause announcement triggered a strong market rally, but EHLS continued to outperform as the S&P 500 flatlined post the announcement.

Mixed Economic Data: GDP and ADP job data showed some softening, but these developments don't impact the fund's investment strategy, which remains focused on sector rotation and strategic positioning.

Low Net Equity: Despite continued market uncertainty, EHLS is confidently positioned with less than 50% net equity exposure, closely monitoring sectors like Utilities and Financials for meaningful adjustments.

Looking Back

The Even Herd Long/Short ETF (EHLS - MKT) outperformed the S&P 500 by a good margin this month, gaining 3.28%, compared to a -1.14% decline in the index. The short side of the portfolio played a critical role in mitigating the extreme market volatility seen in April. With the VIX spiking to levels reminiscent of the financial crisis and pandemic, the short component proved especially beneficial. After years of upward market pressure, shorting has been challenging, but the broad declines earlier this month allowed the fund to reduce drawdown risk effectively.

The announcement of a 90-day tariff pause by President Trump triggered one of the market's strongest days in recent years, with major gains concentrated in mega-cap stocks. Although this rapid price action can be difficult to match due to the fund's broad diversification, EHLS continued to outperform the S&P 500, which has since largely flatlined after the announcement.

The release of GDP data at month-end showed some softening in addition to the ADP job numbers, driven by high import volumes ahead of tariff changes and a reduction in government spending. While this data is noteworthy, it doesn't directly impact our investment decisions. We anticipate similar trends in the next quarter, as this quarter’s GDP did not include events after Liberation Day, as we believe companies that held off on building inventory will likely act if importing from regions where tariffs went on pause.

Looking Forward

As we move into May, we expect ongoing market volatility due to trade negotiations and uncertainty, which will continue to present challenges. However, with improved clustering methodologies we discussed in last month’s update, we are confident in our approach, as evidenced by April's performance.

Sector allocation will likely remain tilted toward Utilities and Financials, with other sectors remaining balanced. We continue to monitor all sectors closely and will adjust when meaningful shifts occur. Currently, Consumer Cyclicals are the most underweight sector, but this could change based on relative performance. However, we do see recently renewed strength in more aggressive utilities such as the independents like Vistra Energy (VST) and NRG Energy (NRG).

In addition, we’ve seen reacceleration in some growth names that were adversely impacted during the market rotation in late February, portfolio names like Sprouts Farmer Markets (SFM), Spotify (SPOT), Carvana (CVNA), Robinhood Markets (HOOD), Netflix (NFLX), and Palantir (PLTR). More speculative areas of the market saw a rather swift drawdown since February, but many of these stocks have traded sideways, such as those with exposure to space or satellite-related industries, as well as quantum computing. Given the amount of uncertainty in the markets, it would have been easy to assume stocks like these should have continued to sell off, but most have not. This continues to make us believe pressures are starting to mount to the upside, but time will tell.

Internationally, we continue to see strength in regions such as Argentina and selective parts of China, and our holdings in global financials, including HSBC (UK), Banco Latinoamericano (BLX, Panama), Mizuho (Japan), and Freedom Holding (Kazakhstan), remain in solid trends. Gold also remains quite strong, which the fund has gold-mining exposure through Agnico Eagle Mines (AEM) and Alamos Gold (AGI). The shift into conservative sectors, notably Utilities and Defensive names, is likely to persist, though we are prepared for potential rotations should trade negotiations progress positively and upside price pressures become more apparent.

While speculation around a new tax plan could serve as a positive catalyst in addition to clarity around trade, we remain cautious on GDP prints, anticipating further softness, at least on paper, given the reasons for its declines—inventory stockpiling and government spending cuts. As of month-end, the fund maintained less than 50% net equity exposure, and we will likely keep this positioning unless major shifts in market conditions warrant an adjustment.

Comments